Empirical Bayes and hierarchical models

K. Friston, W. Penny, in Statistical Parametric Mapping, 2007

The conditional density

Given an estimate of the error covariance of the augmented form Cε and implicitly the priors it entails, one can compute the conditional mean and covariance at each level where the conditional means for each level obtain recursively from:

22.19ηθ|y=E(θ|y)=[ηɛ|y(2)⋮ηɛ|y(n)ηθ|y(n)]ηθ|y(i−1)=E(θ(i−1)y)=X(i)ηθ|y(i)+ηɛ|y(i)

These conditional expectations represent a better characterization of the model parameters than the equivalent ML estimates because they are constrained by higher levels (see summary). However, the conditional mean and ML estimators are the same at the last level. This convergence of classical and Bayesian inference rests on adopting an empirical Bayesian approach and establishes a close connection between classical random effect analyses and hierarchical Bayesian models. The two approaches diverge if we consider that the real power of Bayesian inference lies in coping with incomplete data or unbalanced designs and inferring on the parameters of lower levels. These are the issues considered in the next section.

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/B978012372560850022X

Volume 2

P.D. Wentzell, in Comprehensive Chemometrics, 2009

2.25.3.3.2 Theoretical modeling

An alternative approach to estimating the error covariance matrix by replication is to use fundamental knowledge about the measurement system to build the error covariance matrix. The specific strategy used can range from imposing intuitive knowledge derived from a familiarity with the system under study to more rigorous modeling of the overall measurement system. In the first category, for example, one may have observed that the measurements follow a proportional error structure, or may simply not have as much confidence in one group of measurements compared to another. While MLPCA will only provide truly optimal models if the error structure provided is correct, a feature of the method is that the model will generally become better as information about the error structure is incrementally refined. Therefore, even partial or approximate knowledge of the nature of the noise can be beneficial. Moreover, absolute values for variances and covariances need not be provided since the maximum likelihood projection depends only on the relative values.

In terms of more rigorous modeling of the error structure, a considerable body of knowledge has been developed on the nature of signals from various types of instruments and their limiting sources of noise (e.g., shot noise, source flicker noise, detector noise).16 Such information could be used to develop more refined error information, but there are a couple of limitations to this approach. First, while the instruments may be fairly well characterized, the measurement systems as a whole may introduce some other dominant source of error. For example, assuming that fluorescence measurements are shot-noise limited may be accurate from a signal detection perspective, but the overall error may be dominated by cell positioning, preparation, or sampling errors. A second limitation of this approach is that most noise models have focused on variance and do not tackle the more difficult problem of covariance, which can be tied to specific design factors and signal processing methods.

One special case where theoretical modeling of covariance structure is straightforward is when digital filtering is used. This technique has already been employed in this chapter to generate correlated errors for simulated data. Under these circumstances, the error covariance matrix can be derived directly from the filter. To do this, it is most convenient to describe the filtering process in terms of a filter matrix, F, such that Dfilt = DorigFT, where Dfilt is the filtered data matrix and Dorig is the original data matrix. Typically, F is a band diagonal matrix of filter coefficients, although special considerations have to be made near the edges. Under these conditions, the error covariance matrix for the filtered data will be given by

(81)Σfilt=FΣorigFT

Of course, this still requires a knowledge of the error covariance matrix for the original data, Σorig, but if it can be assumed to be i.i.d. normal, the effect of digital filtering is easy to predict.

The advantages of the theoretical modeling approach are as follows: (1) it eliminates the need for performing replicate measurements; (2) there is no stochastic noise in the error covariance estimates; (3) it is likely to be able to be generalized to all of the measurements made on the same instrument; and (4) the anomalous projection of replicates onto the sample mean is avoided. Unfortunately, coming up with an accurate model on a purely theoretical basis is not likely to be realistic given all of the potential sources of variance and covariance in the noise. Normally, the best that can be hoped for under these circumstances is a model that is better than the assumption of i.i.d. errors. However, another approach is to combine replicate measurements with theoretical modeling, as described in the next section.

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/B9780444527011000570

Selection of Manifest Variables*

Yutaka Kano, in Handbook of Latent Variable and Related Models, 2007

4.1 Model with correlated errors

Probably it was Bollen (1980) who first emphasized importance of introducing error covariances in researches using factor analysis. We shall reanalyze the data set in Section 3.1 to achieve a good fit not by removing manifest variables but by allowing error covariances. We analyzed it with the help of LM tests offered by EQS (Bentler, 2004). The path diagram of a final model is shown in Figure 4. Fit indices of the final model are χ2 = 250.375 (df = 83, n = 653), GFI = 0.950, CFI = 0.952, RMSEA = 0.056. Those statistics indicate a fairly good fit.

Fig. 4. The final model with error covariances.

Recall that SEFA suggests deletion of the variables X2, X9, X13 and X14. We see that SEFA chooses such variables to be removed that those error covariances are eliminated. As a result, the final model with 11 manifest variables is a factor analysis model with uncorrelated errors. This is an interpretation of how SEFA suggests manifest variables to be removed. This gives an answer to question (a). Note that there is some freedom in eliminating error covariances. For example, if either X8 or X9 is removed, the covariance between E8 and E9 can be eliminated. If the model in Figure 4 is true, the choice between X8 and X9 is completely arbitrary from the viewpoint of a model fit. The situation is slightly more complicated for the variables X11 to X14. It is possible to remove three of the four variables. Oka et al. (2002) dropped a total of five variables slightly different from ours by taking into account the meaning of the variables.

There are many cases where it is relevant to introduce error covariances, one of which is the case where there exist confounding third unmeasured variables that connect two or more manifest variables. A method factor is a typical example of confounding variables in studies of social sciences. While common factors cannot usually explain covariances between manifest variables caused by method factors, error covariances can explain them. Method factors are often discussed in the analysis of MTMM matrices (e.g., Campbell and Fiske, 1959; Campbell and O’Connell, 1967).

Green and Hershberger (2000) suggested several kinds of measurement models for longitudinal data. One of their models is a true score model with a moving average component of order one given in Figure 5 (left). The model is equivalent to a one-factor analysis model with errors correlated next to each other (Figure 5 (right)).

Fig. 5. A model with a moving average component of order one and its equivalent model.

A third one is nonlinearity. Suppose that the following nonlinear factor analysis model holds:

X1=μ1+λ11f+λ12f2+e1X2=μ2+λ21f+λ22f2+e2X3=μ3+λ31f+e3⋯Xp=μp+λp1f+ep

where the usual assumptions of a factor analysis model are made. Assuming that the distribution of f1 is symmetric about the origin, we have Cov(f, f2) = 0, and Cov(λ12f2 + e1, λ22f2 + e2) = λ12λ22 Var(f2) (≠ 0) results in an error covariance. When the effect of quadratic terms is not large and does not interest the researcher, one can approximate the effect of f by the linear terms, and the quadratic terms can be regarded as errors. See Lee and Zhu (2002) for general theory of nonlinear structural equation models.

What happens if there exist error covariances in the model and one fits a model without error covariances? A fit of the model will be poor. In addition, factor loadings and communality estimates can be biased. This problem will be discussed in the next section. Which model to employ becomes an issue: a model removing some manifest variables or a model introducing error covariances. We shall discuss this issue in the context of reliability analysis in the next section.

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/B9780444520449500070

The General Linear Model

S.J. Kiebel, … C. Holmes, in Statistical Parametric Mapping, 2007

Estimation of the error covariance matrix

Assuming that the AR(1) + wn is an appropriate model for the fMRI error covariance matrix, we need to estimate three hyperparameters (see Appendix 8.1) at each voxel. The hyperparameterized model gives a covariance matrix at each voxel (Eqn. 8.45). In SPM, an additional assumption is made to estimate this matrix very efficiently, which is described in the following.

The error covariance matrix can be partitioned into two components. The first component is the correlation matrix and the second is the variance. The assumption made by SPM is that the correlation matrix is the same at all voxels of interest (see Chapter 10 for further details).

The variance is assumed to differ between voxels. In other words, SPM assumes that the pattern of serial correlations is the same over all interesting voxels, but its amplitude is different at each voxel. This assumption seems to be quite sensible, because the serial correlations over voxels within tissue types are usually very similar. The ensuing estimate of the serial correlations is extremely precise because one can pool information from the subset of voxels involved in the estimation. This means the correlation matrix at each voxel can be treated as a known and fixed quantity in subsequent inference.

The estimation of the error covariance matrix proceeds as follows. Let us start with the linear model for voxel k:

where Yk is an N × 1 observed time-series vector at voxel k, X is an N × L design matrix, βk is the parameter vector and ek is the error at voxel k. The error ɛk is normally distributed with ɛ˜N(0,σk2V) The critical difference, in relation to Eqn. 8.6, is the distribution of the error; where the identity matrix I is replaced by the correlation matrix V. Note that V does not depend on the voxel position k, i.e. as mentioned above we assume that the correlation matrix V is the same for all voxels k = 1, …, K. However, the variance σk2 is different for each voxel.

Since we assume that V is the same at each voxel, we can pool data from all voxels and then estimate V on this pooled data. The pooled data are given by summing the sampled covariance matrix of all interesting voxels k, i.e. Vϒ=1/KΣkϒkϒkT Note that the pooled VY is a mixture of two variance components; the experimentally induced variance and the error variance component:

The conventional way to estimate the components of the error covariance matrix Cov(ɛk) = σk2 V is to use restricted maximum likelihood (ReML) (Harville, 1997; Friston et al., 2002). ReML returns an unbiased estimator of the covariance components, while accounting for uncertainty about the parameter estimates. ReML can work with precision or covariance components; in our case we need to estimate a mixture of covariance components. The concept of covariance components is a very general concept that can be used to model all kinds of non-sphericity (see Chapter 10). The model described in Appendix 8.1 (Eqn. 8.44) is non-linear in the hyperparameters, so ReML cannot be used directly. But if we use a linear approximation:

where Ql are N × N components and the λl are the hyperparameters, ReML can be applied. We want to specifyQl such that they form an appropriate model for serial correlations in fMRI data. The default model in SPM is to use two components Q1 and Q2. These are Q1 = IN and:

8.38Q2ij={e−|i−j|:i≠j0:i=j

Figure 8.16 shows the shape of Q1 and Q2.

FIGURE 8.16. Graphical illustration of the two covariance components, which are used for estimating serial correlations. Left: component Q1 that corresponds to a stationary white variance component; right: components Q2 that implements the AR(1) part with an autoregression coefficient of 1/e.

A voxel-wide estimate of V is then derived by re-scaling V such that V is a correlation matrix.

This method of estimating the covariance matrix at each voxel uses the two voxel-wide (global) hyperparameters λ1 and λ2. A third voxel-wise (local) hyperparameter (the variance Σ2) is estimated at each voxel using the usual estimator in a least squares mass-univariate scheme (Worsley and Friston, 1995):

where R is the residual forming matrix. This completes the estimation of the serial correlations at each voxel k. Before we can use these estimates to derive statistical tests, we will consider the highpass filter and the role it plays in modelling fMRI data.

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/B9780123725608500085

Kalman Filters and Nonlinear Filters

Vytas B. Gylys, in Encyclopedia of Physical Science and Technology (Third Edition), 2003

IV.B Square Root Filtering

By far the greatest trouble spot in computer mechanization of the KF is the updating of state error covariance matrix P, that is, the computation of Pk∣k according to Eq. (18). As the estimation process progresses, the elements of Pk∣k typically continue to decrease in magnitude and so matrix Pk∣k keeps approaching the zero matrix, although theoretically it should forever remain positive definite, no matter how small in magnitude its elements become. Hence, unless special measures are taken, accumulation of roundoff error in the repetitive use of Eq. (18) may cause the computed Pk∣k to lose its positive definiteness. As suggested by the matrix inversion operation appearing on the right-hand side of Eq. (16) for computing the Kalman gain, this situation is aggravated if several components of the measurement vector are very accurate and consequently the positive definite measurement error covariance matrix R is ill conditioned, that is, if R has eigenvalues of both relatively very large and small magnitudes.

Let A be a nonnegative definite symmetric matrix; then there exists a matrix S such that A = SST. Matrix S is often called the square root of A. The Cholesky decomposition algorithm provides a method of constructing from A the matrix S so that S is lower triangular; that is, all elements of S above the main diagonal are zero. Square root filtering is motivated by the observations that, if the state error covariance matrix P = SST, then (a) since SST is always nonnegative definite, matrix P expressed as SST cannot become negative definite, and (b) matrix S is generally less ill conditioned than matrix P.

Several versions of the square root filtering algorithm are known. The earliest form was developed by J. E. Potter in 1964 for applications in which the process noise is absent (i.e., covariance matrix Q is zero) and the measurements are sequentially processed as scalars. In 1967 J. F. Bellantoni and K. W. Dodge extended Potter’s results to vector-valued measurements. A. Andrews in 1968 and then S. F. Schmidt in 1970 published two alternative procedures for handling the process noise. In 1973 N. A. Carlson described a procedure that considerably improved the speed and decreased the memory requirements of square root filtering and in which, as in Potter’s algorithm, vector-valued measurements are processed sequentially as scalars. Finally, the so-called UDUT covariance factorization method is the most recent major milestone in numerical handling of KFs. This method, developed by G. J. Bierman and C. L. Thornton, represents the state error covariances before and after the measurement update step asPk|k−1=Uk|k−1Dk|k−1Uk|k−1TandPk|k=Uk|kDk|kUk|kT,with D being a diagonal matrix and U an upper triangular matrix with 1’s on its main diagonal. In this method, the square root of the covariance matrix, which now would correspond to UD1/2, is never computed explicitly, which avoids numerical computation of square roots. Like Carlson’s algorithm, the UDUT factorization method maintains the covariance matrix in factored form and so (like Carlson’s algorithm) is considerably more efficient in processor time and storage than the original Potter algorithm.

As a quick comparison of computational efficiency, the conventional Kalman method, the less efficient form of Carlson’s algorithm, and the UDUT factorization method are roughly equal: The processing of each time step (consisting of one time propagation and one measurement update) requires of the order of 16[9ns3 + 9ns2nm + 3ns2nw] adds and about the same number of multiplies, plus a relatively modest number of divides and square roots (square roots are required only in some, as in Potter’s or Carlson’s square root algorithms). Here, as before, ns is the length of the state vector, nm the length of the measurement vector, and nw the lenght of the process noise vector w. The faster version of Carlson’s algorithm is more efficient and requires only of the order of 16[5ns3 + 9ns2nm + 3ns2nw] adds and 16[5ns3 + 12ns2nm + 3ns2nw] multiplies, plus 2nsnm divides and nsnm square roots, at each time point. The stable (Joseph) form of the KF [as given by Eq. (18′)] fares more poorly: At each time step, it requires of the order of 16[18ns3 + 15ns2nm + 3ns2nw] adds and about the same number of multiplies.

As a summary, (a) a square root filter is a numerically stable form for performing the KF covariance–gain processing defined by Eqs. (15), (16), and (18); (b) the efficiency of its more recent versions roughly compares with that of these three equations; (c) the increased stability allows one to use relatively low-precision arithmetic in the KF gain–covariance processing, with a possible exception of some dot products.

Real-time implementation of a filter involves additional issues that are unimportant in the non-real-time environment. Besides the adequacy of functional performance, the most important of these issues is the requirement to produce timely responses to external stimuli. Thus, resorting to a parallel or concurrent processing may be the only way out. This usually implies the use of special hardware architectures such as parallel, vector pipelined, or systolic processors.

As one example, consider the use of a filter in the tracking of multiple objects in a hard real-time environment characterized by strict deadlines. In such a case one may want to maintain simultaneously many estimation processes, each handling a single object. Parallel processors may seem to be a suitable hardware architecture for this problem, but if separate estimation processes in such an application progress at different rates and at any time some of them require a great amount of special handling, then parallel architecture, such as a single-instruction multiple-data stream computer, may not be the best choice. As another example, consider a KF to be implemented as part of a navigation system on a small airborne computer (uniprocessor). Suppose that the navigation measurements come at a certain fixed rate. If the filtering process cannot keep up with the arrival rate of measurements and so not all of them can be utilized, the estimation performance may deteriorate. In this problem, if there is an upper bound on hardware resources, the only solution may be to decompose the estimation algorithm into concurrently executable processes. For instance, the time-propagation step (which, say, is to be executed at a relatively high rate) may constitute one process and the measurement-update step (which needs to be executed only at some lower rate, say, at the rate of measurement arrivals) may constitute another. Such a decomposition of an estimation algorithm into concurrent procedures often creates a surrogate algorithm that performs more poorly than the original algorithm.

The effects of the finite-length word computing is another issue that must be considered in filter implementation for real-time applications. The computer on which a filter is developed and validated through successive off-line simulations is often more powerful and uses higher-precision arithmetic and number representations than the ultimate real-time processor. Hence, one must in advance determine in advance what effect a shorter word length will have on performance.

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/B0122274105003574

Bayesian model selection and averaging

W.D. Penny, … N. Trujillo-Barreto, in Statistical Parametric Mapping, 2007

Variance components

Bayesian estimation, as described in the previous section, assumed that we knew the prior covariance, Cp, and error covariance, Ce. This information is, however, rarely available. In Friston et al. (2002)) these covariances are expressed as:

where Qi and Qj are known as ‘covariance components’ and λi, λj are hyperparameters. Chapter 24 and Friston et al. (2002)) show how these hyperparameters can be estimated using parametric empirical Bayes (PEB). It is also possible to represent precision matrices, rather than covariance matrices, using a linear expansion as shown in Appendix 4.

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/B9780123725608500358

Special Volume: Computational Methods for the Atmosphere and the Oceans

Jacques Blum, … I. Michael Navon, in Handbook of Numerical Analysis, 2009

7.13 Covariance localization

One aspect of ensemble assimilation methods is the requirement of accuracy for covariance matrices. Erroneous representation of error statistics affects the analysis-error covariance, which is propagated forward in time.

The covariance estimate from the ensemble is multiplied point by point with a correlation function that is 1.0 at the observation location and zero beyond some prespecified distance (correlation length).

Two approaches are used: one consists in a cut-off radius so that observations are not assimilated beyond a certain distance from the grid point (see Houtekamer and Mitchell [1998], Evensen [2003]). This may introduce spurious discontinuities.

The second approach is to use a correlation function that decreases monotonically with increasing distance. This results in the Kalman gain

(7.25)K=PbHT(HPbHT+R)−1,

being replaced by a modified gain

(7.26)K=(ρsоPb)HT(H(ρsоPb)HT+R)−1,

where the operation ρsо denotes a Schur product (an element-by-element multiplication) of a correlation matrix S with local support with the covariance model generated by the ensemble. The Schur product of matrices A and B is a matrix C of the same dimension, where cij= aijbij. When covariance localization is applied to smaller ensembles, it may result in more accurate analyses than would be obtained from larger ensembles without localization Houtekamer and Mitchell [2001]. Localization increases the effective rank of the background error covariances Hamill, Whitaker and Snyder [2001].

Generally, the larger the ensemble, the broader the optimum correlation length scale of the localization function (Houtekamer and Mitchell [2001], Hamill, Whitaker and Snyder [2001]). See Whitaker, Compo, Wei and Hamill [2004] and Houtekamer, Mitchell, Pellerin, Buehner, Charron, Spacek and Hansen [2005] for examples performing ensemble assimilations that also include a vertical covariance localization.

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/S1570865908002093

Random Effects Analysis

W.D. Penny, A.J. Holmes, in Statistical Parametric Mapping, 2007

Unbalanced designs

The model described in this section is identical to the separable model in the previous chapter, but with xi = 1ni. If the error covariance matrix is non-isotropic, i.e. C ≠ σ2wI then the population estimates will change. This can occur, for example, if the design matrices are different for different subjects (so-called unbalanced-designs), or if the data from some of the subjects are particularly ill-fitting. In these cases, we consider the within-subject variances σ2w(i) and the number of events ni to be subject-specific. This will be the case in experimental paradigms where the number of events is not under experimental control, e.g. in memory paradigms where ni may refer to the number of remembered items.

If we let M = 1N, then the second level in Eqn. 11.2 in the previous chapter is the matrix equivalent of the second-level in Eqn. 12.14 (i.e. it holds for all i). Plugging in our values for M and X gives:

12.20Var[wˆpop]=(∑i=1Nαβiniα+niβi)−1

and

12.21wˆpop=(∑i=1Nαβiniα+niβi)−1∑i=1Nαβiα+βini∑j=1niyij

This reduces to the earlier result if βi = β and ni = n. Both of these results are different to the summary-statistic approach, which we note is therefore mathematically inexact for unbalanced designs. But as we shall see in the numerical example below, the summary-statistic approach is remarkably robust to departures from assumptions about balanced designs.

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/B9780123725608500127

Predictive variable structure filter

Lu Cao, … Bing Xiao, in Predictive Filtering for Microsatellite Control System, 2021

7.6 State estimation error covariance of PSVSF

Although the implementation of Algorithms 7.1–7.3 does not need the calculation of the covariance, which is to be computed in this section for evaluating the filtering performance.

Taking Algorithm 7.3 as an example, the states estimation process of the PSVSF can be written into the following Kalman filtering form.

(7.34)xˆk+1/k=f(xˆk)

(7.35)xˆk+1=xˆk+1/k+g(xˆk)(U(xˆk))−1diag(|eyk+1/k|+γ|eyk|)sat(|eyk+1/k|ℓ)

or

(7.36)xˆk+1=xˆk+1/k+Kk+1eyk+1/k

(7.37)Kk+1=gU(xˆk)diag(|eyk+1/k|+γ|eyk|)diag(sat(|eyk+1/k|ℓ))×(diag(eyk+1/k))−1

where gU(xˆk)=g(xˆk)(U(xˆk))−1. Here, Kk+1 is defined as the gain matrix of the modeling error.

Based on (7.36)–(7.37), let x˜xk+1/k=xk+1−xˆk+1/k be the prior state estimation error, then we have

(7.38)x˜xk+1/k=xk+1−xˆk+1/k=f(xk)−f(xˆk)=Fkx˜k/k

where Fk=∂f∂x|x=xk and x˜xk/k=xk−xˆk/k.

Using the definition of the prior covariance of state estimation error, it follows that

(7.39)Px˜,k+1/k=E(x˜k+1/kx˜k+1/kT)=FkE(x˜k/kx˜k/kT)FkT=FkPx˜,kFkT

(7.40)Px˜,k+1=E(x˜k+1x˜k+1T)

with x˜k+1=xk+1−xˆk+1. Then, invoking (7.36)–(7.37) results in

(7.41)x˜k+1=xk+1−xˆk+1/k−Kk+1eyk+1/k=x˜k+1/k−Kk+1(yk+1−yˆk−Z(xˆk))=x˜k+1/k−Kk+1(h(xk+1)+vk+1−h(xˆk+1/k))=x˜k+1/k−Kk+1(Hxˆk+1/k+vk+1)=(In−Kk+1Hk+1)xˆk+1/k−Kk+1vk+1

Combining (7.40) and (7.41), applying the fact that the measurement noise vk+1 has zero mean, then the state estimation error covariance Px˜,k+1 achieved by the PSVSF can be calculated as

(7.42)Px˜,k+1=E(xaxaT)=(In−Kk+1Hk+1)Px˜,k+1/k(In−Kk+1Hk+1)T+Kk+1Rk+1KK+1T

where xa=(In−Kk+1Hk+1)xˆk+1/k−Kk+1vk+1.

Based on the above analysis, the covariance estimation included version of the PSVSF can be presented in Algorithm 7.4. Moreover, the numerical integral method is adopted to update the state and the output estimation in Algorithm 7.4.

Algorithm 7.4. Covariance estimation included PSVSF.

Remark 7.4

When applying the PSVSF into practical engineering, updating the estimation of the modeling error and updating the state estimation should be executed only, while updating the error covariance is not necessary. Hence, the implementation of the PSVSF demands fewer computer resources. It has great practical application potential. Moreover, it is very appropriate to solve the state estimation problem of the systems with limited computation power.

Remark 7.5

The linearization technique is applied to estimate Px˜,k+1/k. This may affect the estimation accuracy of the covariance Px˜,k+1/k. To avoid this shortcoming, the sigma-points schemes in Part II can be applied to improve the covariance’s estimation accuracy, those procedures are listed as follows.

- •

-

Method #1: UT-based estimation. When implementing this method, let us first calculate

(7.43)Px˜,k=SkSkT=∑i=1nσi,kσi,kT

(7.44)ξ0,k=xˆk,W0=κn+κ

(7.45)Wj=12(n+κ),j=1,2,3,⋯,2n

(7.46)ξi,k=xˆk+n+κσi,k,i=1,2,3,⋯,n

(7.47)ξi+n,k=xˆk−n+κσi,k

(7.48)xˆi,k+1/k=f(ξi,k),i=1,2,3,⋯,2n

then updating the state estimation error covariance by using

(7.49)Px˜,k+1/k=∑i=02nWi(xˆi,k+1/k−xˆk+1/k)(xˆi,k+1/k−xˆk+1/k)T

(7.50)Px˜,k+1=(In−Kk+1Hk+1)Px˜,k+1/k(In−Kk+1Hk+1)T+Kk+1Rk+1Kk+1T

- •

-

Method #2: Cubature rule-based estimation. The following calculations are first conducted to execute this filtering method.

(7.51)Px˜,k=SkSkT=∑i=0nσi,kσi,kT

(7.52)ξi,k=xˆk+nσi,k,i=1,2,3,⋯,n

(7.53)ξi+n,k=xˆk−nσi,k,i=1,2,3,⋯,n

(7.54)xˆi,k+1/k=f(ξi,k),i=0,1,2,⋯,2n

Then, updating the state estimation error covariance by using

(7.55)Px˜,k+1/k=12n∑i=02n(xˆi,k+1/kxˆi,k+1/kT−xˆk+1/kxˆk+1/kT)

(7.56)Px˜,k+1=(In−Kk+1Hk+1)Px˜,k+1/k(In−Kk+1Hk+1)T+Kk+1Rk+1Kk+1T

- •

-

Method #3: Stirling’s polynomial interpolation-based estimation. For this method, the following calculations are carried out first.

(7.57)Px˜,k=SkSkT=∑i=1nσi,kσi,kT

(7.58)ξ0,k=xˆk,ξi,k=xˆk+hσi,k,i=1,2,3,⋯,n

(7.59)ξi+n,k=xˆk−hσi,k,i=1,2,3,⋯,n

Then, updating the state estimation error covariance by using

(7.60)Px˜,k+1/k=14h2∑i=02n(f(ξi,k)−f(ξi+n,k))2+h2−14h4∑i=02n(f(ξi,k)−f(ξi+n,k)−2f(ξ0,k))2

(7.61)Px˜,k+1=(In−Kk+1Hk+1)Px˜,k+1/k(In−Kk+1Hk+1)T+Kk+1Rk+1Kk+1T

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/B978012821865500022X

Unscented predictive filter

Lu Cao, … Bing Xiao, in Predictive Filtering for Microsatellite Control System, 2021

4.4 Covariance constraint analysis

For the classical PF, the optimal state estimation is determined based on the assumption that the consistent estimations of the states must match the available measurements with a residual error covariance which is approximately equal to the known measurement error covariance. This necessary condition is hereafter referred to as the “covariance constraint”. The covariance constraint is imposed by requiring the following approximation to be satisfied:

(4.58)E((yk−h(xˆk))(yk−h(xˆk))T)=Rˆk≈Rk,k=1,2,⋯,ς

where ς∈N denotes the number of the set of measurements. This means that the estimated output h(xˆk) is required to fit the actual measurements yk with approximately the same error covariance as the actual measurements fit the truth. Otherwise, the estimation is statistically inconsistent.

Theoretically, the optimal weighting matrix WE of any filtering algorithms should be chosen with covariance constraint (4.58) satisfied. Hence, there is a balance between the modeling error and the residual error of estimation. When the covariance constraint is not satisfied, then choosing the optimal weighting matrix WE and compensating for the modeling error should be done simultaneously to ensure Rˆk→Rk. In this case, it is difficult to determine the optimal weighting matrix WE. Note that WE is constantly chosen based on the experience of engineers.

Based on (2.64) and (4.25), it follows that

(4.59)E((yk−h(xˆk))(yk−h(xˆk))T)=Rk=E(∑i=1∞∑j=1∞1i!j!(DΔxih)(DΔxjh)T︸condition_1)−E(DΔx2h2!)E((DΔx2h2!)T)−E(∑i=1∞∑j=1∞1(2i)!(2j)!DΔx2ih(DΔx2jh)T︸condition_2)+GhPx˜,kGhT

(4.60)E((yk−h((xˆk)PF))(yk−h((xˆk)PF))T)=(Rˆk)PF=GhPx˜,kGhT

(4.61)E((yk−h((xˆk)UPF))(yk−h((xˆk)UPF))T)=(Rˆk)UPF=GhPx˜,kGhT−E(DΔx2h2!)E((DΔx2h2!)T)+1n+κ∑m=1n∑i=1∞∑j=1∞1i!j!(Dσˆkmih)(Dσˆkmjh)T︸condition_1−∑m=1n∑i=1∞∑j=1∞1(2i)!(2j)!(n+κ)2∑l=1n∑p=1n1(2i)!(2j)!Dσˆkl2ih(Dσˆkp2jh)T︸condition_1

It is found in (4.59)–(4.61) that the covariance of the estimation error achieved by the PF is only accurate to the second-order accuracy of the real value. The covariance of the estimation error achieved by the UPF is accurate to the fourth-order accuracy of the real value. Hence, (Rˆk)UPF is more consistent with Rk than (Rˆk)PF. This implies that the selection of the weighting matrix WE for the UPF depends less on the covariance constraint. The UPF has more freedom to choose WE. Hence, the practical application value of the UPF is great than the classical PF.

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/B9780128218655000188

В предыдущих параграфах данной главы мы рассматривали случай отказа от одной предпосылки классической линейной модели множественной регрессии. Теперь мы расширим наш анализ и откажемся сразу от двух предпосылок: от предпосылок №№4-5 (о постоянстве дисперсии случайной ошибки и о некоррелированности разных случайных ошибок между собой). В техническом смысле этот параграф несколько сложнее предыдущих (в частности, тут более широко используется линейная алгебра). Поэтому, если вы заинтересованы в том, чтобы разобраться только в прикладных аспектах множественной регрессии, а в соответствующих вычислениях готовы полностью довериться эконометрическому пакету, можете его пропустить.

Отказ от указанных двух предпосылок означает, что ковариационная матрица вектора случайных ошибок (таблица, в которой записаны все ковариации между (varepsilon_{i}) и (varepsilon_{j}), см. параграф 3.3) больше не является диагональной матрицей с одинаковыми числами на главной диагонали, как это было в первоначальной классической модели. Теперь ковариационная матрица вектора случайных ошибок Ω — это произвольная ковариационная матрица (разумеется, так как это не совсем любая матрица, а именно ковариационная матрица, то по своим свойствам она является симметричной и положительно определенной).

Модель, в которой сохранены только первые три предпосылки классической линейной модели множественной регрессии, называется обобщенной линейной моделью множественной регрессии.

Проанализируем, к каким последствиям приводит отказ от предпосылок №№4-5.

Во-первых, полученная обычным методом наименьших квадратов оценка ({widehat{beta} = left( {X^{‘}X} right)^{- 1}}X’y) остается несмещенной (это свойство мы доказывали, опираясь как раз лишь на первые три предпосылки).

Во-вторых, МНК-оценки хоть и остаются несмещенными, но больше не являются эффективными.

В-третьих, если мы оцениваем ковариационную матрицу вектора оценок коэффициентов (которая нужна для тестирования всевозможных гипотез), то оценка (widehat{V}{{(widehat{beta})} = left( {X^{‘}X} right)^{- 1}}S^{2}) смещена и больше не является корректной.

Чтобы убедиться в этом, посчитаем ковариационную матрицу от (widehat{beta}) в условиях обобщенной модели (при этом мы используем свойства ковариационной матрицы, перечисленные в параграфе 3.3):

(V{left( widehat{beta} right) = V}{leftlbrack {{({X^{‘}X})}^{- 1}X’y} rightrbrack = V}{leftlbrack {{({X^{‘}X})}^{- 1}X'{({mathit{Xbeta} + varepsilon})}} rightrbrack =})

({}V{leftlbrack {{({{({X^{‘}X})}^{- 1}X’})}varepsilon} rightrbrack = left( {X^{‘}X} right)^{- 1}}X^{‘}Vlbrackvarepsilonrbrack{left( {left( {X^{‘}X} right)^{- 1}X^{‘}} right)^{‘} = {({X^{‘}X})}^{- 1}}X^{‘}Omega{left( {left( {X^{‘}X} right)^{- 1}X^{‘}} right)^{‘} = {({X^{‘}X})}^{- 1}}X^{‘}Omega X{({X^{‘}X})}^{- 1})

Так выглядит ковариационная матрица вектора МНК-оценок в обобщенной модели. Ясно, что она не может быть корректно оценена стандартной оценкой (left( {X^{‘}X} right)^{- 1}S^{2}). Следовательно, прежней формулой пользоваться нельзя: если мы будем использовать стандартные ошибки, рассчитанные по обычной формуле (предполагая выполнение предпосылок классической линейной модели), то получим некорректные стандартные ошибки, что может привести нас к неверным выводам по поводу значимости или незначимости тех или иных регрессоров.

Таким образом, последствия перехода к обобщенной модели аналогичны тем, что мы наблюдали для случая гетероскедастичности. Это неудивительно, так как гетероскедастичность — частный случай обобщенной линейной модели.

Поэтому для получения эффективных оценок обычный МНК не подойдет, и придется воспользоваться альтернативным методом — обобщенным МНК (ОМНК, generalized least squares, GLS). Формулу для расчета оценок коэффициентов при помощи ОМНК позволяет получить специальная теорема.

Теорема Айткена

Если

- модель линейна по параметрам и правильно специфицирована

({y = {mathit{Xbeta} + varepsilon}},) - матрица Х — детерминированная матрица, имеющая максимальный ранг k,

- (E{(varepsilon) = overrightarrow{0}}),

- (V{(varepsilon) = Omega}) — произвольная положительно определенная и симметричная матрица,

то оценка вектора коэффициентов модели ({{widehat{beta}}^{} = {({X’Omega^{- 1}X})}^{- 1}}X’Omega^{- 1}y) является:

- несмещенной

- и эффективной, то есть имеет наименьшую ковариационную матрицу в классе всех несмещенных и линейных по y оценок.

Предпосылки теоремы Айткена — это предпосылки обобщенной линейной модели множественной регрессии. Из них первые три — стандартные, как в классической модели, а четвертая ничего особого не требует (у вектора случайных ошибок может быть любая ковариационная матрица без каких-либо дополнительных специальных ограничений). Сама теорема Айткена является аналогом теоремы Гаусса — Маркова для случая обобщенной модели.

Докажем эту теорему.

Из линейной алгебры известно: если матрица (Omega) симметрична и положительно определена, то существует такая матрица P, что

(P’bullet{P = Omega^{- 1}}) ⇔ ({P^{‘} = Omega^{- 1}}bullet P^{- 1})

А раз такое представление возможно, то воспользуемся им для замены переменных. От вектора значений зависимой переменной (y), перейдем к вектору (Pbullet y), обозначив его как вектор ({y^{} = P}bullet y). Аналогичным образом введем матрицу ({X^{} = P}bullet X) и вектор ошибок ({varepsilon^{} = P}bulletvarepsilon).

Вернемся к исходной модели, параметры которой нас и интересуют:

({y = X}{beta + varepsilon})

Умножим левую и правую части равенства на матрицу (P):

({mathit{Py} = mathit{PX}}{beta + mathit{Pvarepsilon}})

С учетом новых обозначений это равенство можно записать так:

({y^{} = X^{}}{beta + varepsilon^{}})

Для новой модели (со звездочками) выполняются предпосылки теоремы Гаусса-Маркова. Чтобы в этом убедиться, достаточно показать, что математическое ожидание вектора случайных ошибок является нулевым вектором (третья предпосылка классической модели) и ковариационная матрица вектора случайных ошибок является диагональной с одинаковыми элементами на главной диагонали (четвертая и пятая предпосылки).

Для этого вычислим математическое ожидание нового вектора ошибок:

(E{left( varepsilon^{} right) = E}{left( mathit{Pvarepsilon} right) = P}bullet E{(varepsilon) = P}bullet{overrightarrow{0} = overrightarrow{0}})

Теперь вычислим ковариационную матрицу вектора (varepsilon^{}):

(V{left( varepsilon^{} right) = V}{left( {Pbulletvarepsilon} right) = P}bullet V(varepsilon)bullet{P^{‘} = P}bulletOmegabullet{P^{‘} = P}bulletOmegabulletOmega^{- 1}bullet{P^{- 1} = I_{n}})

Здесь (I_{n}) обозначает единичную матрицу размера n на n.

Следовательно, для модели со звездочками выполняются все предпосылки теоремы Гаусса — Маркова. Поэтому получить несмещенную и эффективную оценку вектора коэффициентов можно, применив к этой измененной модели обычный МНК:

({{widehat{beta}}^{} = left( {{X^{}}^{‘}X^{}} right)^{- 1}}{X^{}}^{‘}y^{})

Теперь осталось вернуться к исходным обозначениям, чтобы получить формулу несмещенной и эффективной оценки интересующего нас вектора в терминах обобщенной модели:

({{widehat{beta}}^{} = left( {{X^{}}^{‘}X^{}} right)^{- 1}}{X^{}}^{‘}{y^{} = left( {{(mathit{PX})}^{‘}mathit{PX}} right)^{- 1}}left( mathit{PX} right)^{‘}{mathit{Py} = left( {X’P’mathit{PX}} right)^{- 1}}X^{‘}P^{‘}{mathit{Py} =}left( {X’Omega^{- 1}P^{- 1}mathit{PX}} right)^{- 1}X’Omega^{- 1}P^{- 1}{mathit{Py} = {({X’Omega^{- 1}X})}^{- 1}}X’Omega^{- 1}y)

Что и требовалось доказать.

Взвешенный МНК, который мы обсуждали ранее, — это частный вариант обобщенного МНК (для случая, когда только предпосылка №4 нарушена, а предпосылка №5 сохраняется).

Как и при использовании взвешенного МНК в ситуации применения ОМНК коэффициент R-квадрат не обязан лежать между нулем и единицей и не может быть интерпретирован стандартным образом.

Слабая сторона ОМНК состоит в том, что для его реализации нужно знать не только матрицу регрессоров X с вектором значений зависимой переменной y, но и ковариационную матрицу вектора случайных ошибок (Omega). На практике, однако, эта матрица почти никогда не известна. Поэтому в прикладных исследованиях практически всегда вместо ОМНК используется, так называемый, доступный ОМНК (его ещё называют практически реализуемый ОМНК, feasible GLS). Идея доступного ОМНК состоит в том, что следует сначала оценить матрицу (Omega) (традиционно обозначим её оценку (widehat{Omega})), а уже затем получить оценку вектора коэффициентов модели, заменив в формуле ОМНК (Omega) на (widehat{Omega}):

({{widehat{beta}}^{} = {({X'{widehat{Omega}}^{- 1}X})}^{- 1}}X'{widehat{Omega}}^{- 1}y.)

Применение этого подхода осложняется тем, что (widehat{Omega}) не может быть оценена непосредственно без дополнительных предпосылок, так как в ней слишком много неизвестных элементов. Действительно, в матрице размер (n) на (n) всего (n^{2}) элементов, и оценить их все, имея всего (n) наблюдений, представляется слишком амбициозной задачей. Даже если воспользоваться тем, что матрица (Omega) является симметричной, в результате чего достаточно оценить только элементы на главной диагонали и над ней, мы все равно столкнемся с необходимостью оценивать (left( {n + 1} right){n/2}) элементов, что всегда больше числа доступных нам наблюдений.

Поэтому процедура доступного ОМНК устроена так:

- Делаются некоторые предпосылки по поводу того, как устроена ковариационная матрица вектора случайных ошибок (Omega). На основе этих предпосылок оценивается матрица (widehat{Omega}).

- После этого по формуле ({({X'{widehat{Omega}}^{- 1}X})}^{- 1}X'{widehat{Omega}}^{- 1}y) вычисляется вектор оценок коэффициентов модели.

Из сказанного следует, что доступный ОМНК может быть реализован только в ситуации, когда есть разумные основания сформулировать те или иные предпосылки по поводу матрицы (widehat{Omega}). Рассмотрим некоторые примеры таких ситуаций.

Пример 5.4. Автокорреляция и ОМНК-оценка

Рассмотрим линейную модель ({y = X}{beta + varepsilon}), для которой дисперсия случайных ошибок постоянна, однако наблюдается так называемая автокорреляция первого порядка:

(varepsilon_{i} = {{rho ast varepsilon_{i — 1}} + u_{i}})

Здесь (u_{i}) — независимые и одинаково распределенные случайные величины с дисперсией (sigma_{u}^{2}), а (rhoin{({{- 1},1})}) — коэффициент автокорреляции.

(а) Найдите ковариационную матрицу вектора случайных ошибок для представленной модели.

(б) Запишите в явном виде формулу ОМНК-оценки вектора коэффициентов модели, предполагая, что коэффициент (rho) известен.

Примечание: в отличие от гетероскедастичности, автокорреляция случайных ошибок обычно наблюдается не в пространственных данных, а во временных рядах. Для временных рядов вполне естественна подобная связь будущих случайных ошибок с предыдущими их значениями.

Решение:

(а) Используя условие о постоянстве дисперсии случайной ошибки, то есть условие (mathit{var}{{(varepsilon_{i})} = mathit{var}}{(varepsilon_{i — 1})}), найдем эту дисперсию:

(mathit{var}{{(varepsilon_{i})} = mathit{var}}{({{rho ast varepsilon_{i — 1}} + u_{i}})})

(mathit{var}{{(varepsilon_{i})} = rho^{2}}mathit{var}{{(varepsilon_{i — 1})} + mathit{var}}{(u_{i})})

(mathit{var}{{(varepsilon_{i})} = rho^{2}}mathit{var}{{(varepsilon_{i})} + sigma_{u}^{2}})

(mathit{var}{left( varepsilon_{i} right) = frac{sigma_{u}^{2}}{1 — rho^{2}}}.)

Тем самым мы нашли элементы, которые будут стоять на главной диагонали ковариационной матрицы вектора случайных ошибок. Теперь найдем элементы, которые будут находиться непосредственно на соседних с главной диагональю клетках:

(mathit{cov}{left( {varepsilon_{i},varepsilon_{i — 1}} right) = mathit{cov}}{left( {{{rho ast varepsilon_{i — 1}} + u_{i}},varepsilon_{i — 1}} right) = {rho ast mathit{cov}}}{left( {varepsilon_{i — 1},varepsilon_{i — 1}} right) + mathit{cov}}{left( {u_{i},varepsilon_{i — 1}} right) = {rho ast mathit{var}}}{{left( varepsilon_{i — 1} right) + 0} = frac{rho ast sigma_{u}^{2}}{1 — rho^{2}}})

По аналогии легко убедиться, что

(mathit{cov}{left( {varepsilon_{i},varepsilon_{i — k}} right) = frac{rho^{k} ast sigma_{u}^{2}}{1 — rho^{2}} = frac{sigma_{u}^{2} ast rho^{k}}{1 — rho^{2}}}.)

Следовательно, ковариационная матрица вектора случайных ошибок имеет вид:

({Omega = frac{sigma_{u}^{2}}{1 — rho^{2}}}begin{pmatrix} begin{matrix} 1 & rho \ rho & 1 \ end{matrix} & ldots & begin{matrix} rho^{n — 2} & rho^{n — 1} \ rho^{n — 3} & rho^{n — 2} \ end{matrix} \ ldots & ldots & ldots \ begin{matrix} rho^{n — 2} & rho^{n — 3} \ rho^{n — 1} & rho^{n — 2} \ end{matrix} & ldots & begin{matrix} 1 & rho \ rho & 1 \ end{matrix} \ end{pmatrix})

(б) Вектор ОМНК-оценок коэффициентов имеет вид:

({{widehat{beta}}^{} = {({X’Omega^{- 1}X})}^{- 1}}X^{‘}Omega^{- 1}{y =}{left( {X’begin{pmatrix} begin{matrix} 1 & rho \ rho & 1 \ end{matrix} & ldots & begin{matrix} rho^{n — 2} & rho^{n — 1} \ rho^{n — 3} & rho^{n — 2} \ end{matrix} \ ldots & ldots & ldots \ begin{matrix} rho^{n — 2} & rho^{n — 3} \ rho^{n — 1} & rho^{n — 2} \ end{matrix} & ldots & begin{matrix} 1 & rho \ rho & 1 \ end{matrix} \ end{pmatrix}^{- 1}X} right)^{- 1} ast}X’begin{pmatrix} begin{matrix} 1 & rho \ rho & 1 \ end{matrix} & ldots & begin{matrix} rho^{n — 2} & rho^{n — 1} \ rho^{n — 3} & rho^{n — 2} \ end{matrix} \ ldots & ldots & ldots \ begin{matrix} rho^{n — 2} & rho^{n — 3} \ rho^{n — 1} & rho^{n — 2} \ end{matrix} & ldots & begin{matrix} 1 & rho \ rho & 1 \ end{matrix} \ end{pmatrix}^{- 1}y)

Обратите внимание, что дробь (frac{sigma_{u}^{2}}{1 — rho^{2}}) при расчете представленной оценки сокращается. Поэтому для вычисления оценки знать величину (sigma_{u}^{2}) не нужно.

Примечание: если коэффициент автокорреляции (rho) неизвестен, то его можно легко оценить. Например, для этого можно применить обычный МНК к исходной регрессии, получить вектор остатков и оценить регрессию ({widehat{e}}_{i} = {widehat{rho} ast e_{i — 1}}). Полученной оценки (widehat{rho}) достаточно, чтобы вычислить ОМНК-оценку вектора параметров модели. Тем самым в представленном примере для применения доступного ОМНК достаточно оценить всего один параметр ковариационной матрицы вектора оценок коэффициентов.

Пример 5.5. Гетероскедастичность и ОМНК-оценка

Рассмотрим линейную модель ({y = X}{beta + varepsilon}), для которой выполнены все предпосылки классической линейной модели множественной регрессии за одним исключением: дисперсия случайной ошибки прямо пропорциональна квадрату некоторой известной переменной

(mathit{var}{left( varepsilon_{i} right) = sigma_{i}^{2} = sigma_{0}^{2}}{z_{i}^{2} > 0}.)

(а) Найдите ковариационную матрицу вектора случайных ошибок для представленной модели.

(б) Запишите в явном виде формулу ОМНК-оценки вектора коэффициентов модели.

Решение:

(а) Так как в этом случае нарушена только четвертая предпосылка классической линейной модели множественной регрессии, то вне главной диагонали ковариационной матрицы вектора случайных ошибок будут стоять нули.

(Omega = begin{pmatrix} begin{matrix} {sigma_{0}^{2}z_{1}^{2}} & 0 \ 0 & {sigma_{0}^{2}z_{2}^{2}} \ end{matrix} & begin{matrix} ldots & 0 \ ldots & 0 \ end{matrix} \ begin{matrix} ldots & ldots \ 0 & 0 \ end{matrix} & begin{matrix} ldots & ldots \ ldots & {sigma_{0}^{2}z_{n}^{2}} \ end{matrix} \ end{pmatrix})

(б) Обратите внимание, что при подстановке в общую формулу для ОМНК-оценки величина (sigma_{0}^{2}) сокращается, следовательно, для оценки вектора коэффициентов знать её не нужно:

({{widehat{beta}}^{} = {({X’Omega^{- 1}X})}^{- 1}}X^{‘}Omega^{- 1}{y =}left( {X’begin{pmatrix} begin{matrix} z_{1}^{2} & 0 \ 0 & z_{2}^{2} \ end{matrix} & begin{matrix} ldots & 0 \ ldots & 0 \ end{matrix} \ begin{matrix} ldots & ldots \ 0 & 0 \ end{matrix} & begin{matrix} ldots & ldots \ ldots & z_{n}^{2} \ end{matrix} \ end{pmatrix}^{- 1}X} right)^{- 1}X’begin{pmatrix} begin{matrix} z_{1}^{2} & 0 \ 0 & z_{2}^{2} \ end{matrix} & begin{matrix} ldots & 0 \ ldots & 0 \ end{matrix} \ begin{matrix} ldots & ldots \ 0 & 0 \ end{matrix} & begin{matrix} ldots & ldots \ ldots & z_{n}^{2} \ end{matrix} \ end{pmatrix}^{- 1}y)

* * *

Ещё одна важная ситуация, когда с успехом может быть применен доступный ОМНК — это модель со случайными эффектами, которую мы рассмотрим в главе, посвященной панельным данным.

Вариации

оценок параметров будут, в конечном

счете, определять точность уравнения

множественной регрессии. Для их измерения

в многомерном регрессионном анализе

рассматривают так называемую

ковариационную

матрицу К,

являющуюся

матричным аналогом дисперсии одной

переменной:

.

.

где

элементы

ковариации

ковариации

(или

корреляционные

моменты) оценок

параметров

и

и

.

.

Ковариация

двух переменных определяется как

математическое ожидание произведения

отклонений этих переменных от их

математических ожиданий [Ссылка]. Поэтому

, (13.28)

, (13.28)

где

и

и математические

математические

ожидания соответственно для параметров

и

.

.

Ковариация

характеризует как степень рассеяния

значений двух переменных относительно

их математических ожиданий, так и

взаимосвязь этих переменных.

В

силу того, что оценки

,

,

полученные методом наименьших квадратов,

являются несмещенными оценками параметров ,

,

т.е.

,

,

выражение(13.28)

примет

вид:

.

.

Рассматривая

ковариационную матрицу К,

легко

заметить, что на ее главной диагонали

находятся дисперсии опенок параметров

регрессии, ибо

.

.

(13.29)

В

сокращенном виде ковариационная матрица

К

имеет

вид:

.

.

(13.30)

Учитывая

(13.28)

мы

можем записать

.

.

Тогда

выражение (12.30) примет вид:

,

,

(13.31)

ибо

элементы матрицы X

—неслучайные

величины.

Матрица

представляет

собой ковариационную матрицу

вектора возмущений

:

:

в

которой все элементы, не лежащие на

главной диагонали, равны нулю в силу

предпосылки 4

о

некоррелированности возмущений

,

,

и

между

собой,

а

все элементы, лежащие на главной

диагонали, в силу предпосылок 2

и

3

регрессионного

анализа

равны

одной и той же дисперсии

:

:

.

.

Поэтому

матрица

,

,

где

единичная

матрица

го

го

порядка.

Следовательно, в силу (13.31)

ковариационная

матрица вектора

оценок

параметров:

Так

как

и

и

,

,

то окончательно получим:

(13.32)

(13.32)

Таким

образом, с

помощью обратной матрицы нормальных

нормальных

уравнении регрессии

определяется

не только сам вектор

оценок

оценок

параметров (13.28),

но

и дисперсии и ковариации его компонент.

Входящая

в (13.32)

дисперсия

возмущений неизвестна. Заменив ее

выборочной остаточной дисперсией

(13.33)

(13.33)

по

(13.32)

получаем

выборочную оценку ковариационной

матрицы К.

(В

знаменателе выражения (13.33)

стоит

,

,

а

не

,

,

как

это было выше в (13.6).

Это

связано с тем, что теперь

степеней

степеней

свободы (а не две) теряются при определении

неизвестных параметров, число которых

вместе со свободным членом равно

равно .

.

4.10. Определение доверительных интервалов для коэффициентов и функции множественной регрессии

Перейдем

теперь к оценке значимости коэффициентов

регрессии

и

построению доверительного интервала

для параметров регрессионной модели

.

.

В

силу (13.29),

(13.32) и

изложенного выше оценка дисперсии

коэффициента регрессии

определится

по формуле:

где

несмещенная

оценка параметра

;

;

диагональный

диагональный

элемент матрицы

.

.

Среднее

квадратическое отклонение (стандартная

ошибка) коэффициента регрессии

примет

вид:

.

.

(13.34)

Значимость

коэффициента регрессии

можно

проверить, если учесть, что статистика

имеет

имеет распределение

распределение

Стьюдента с

степенями

степенями

свободы. Поэтому

значимо

отличается от нуля на уровне

значимости

,

,

если соответствующий

соответствующий ныйдоверительный

ныйдоверительный

интервал для параметра

есть

.

.

(13.35)

Наряду

с интервальным оцениванием коэффициентов

регрессии по (13.35)

весьма

важным для оценки точности определения

зависимой переменной (прогноза) является

построение доверительного

интервала для функции регрессии или

для условного математического

ожидания зависимой переменной

,

,

найденного в предположении, что

объясняющие переменные

приняли

значения, задаваемые вектором

.Выше

.Выше

такой интервал получен для уравнения

парной регрессии (см. (13.13)

и

(13.12)).

Обобщая

соответствующие выражения на случай

множественной регрессии, можно получить

доверительный интервал для

:

:

где

групповая

групповая

средняя, определяемая по уравнению

регрессии,

(13.36)

(13.36)

— ее

стандартная ошибка.

При

обобщении формул (13.15)

и

(13.14)

аналогичный

доверительный

интервал для индивидуальных значений

зависимой переменной

примет

примет

вид:

(13.37)

(13.37)

где

.

.

(13.38)

Доверительный

интервал для дисперсии возмущений

в

множественной регрессии с надежностью

строится аналогично парной модели

строится аналогично парной модели

по формуле(13.20)

с

соответствующим изменением числа

степеней свободы критерия

:

:

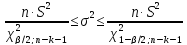

(13.39)

(13.39)

Пример

13.6.

По

данным примера 13.4

оценить

сменную добычу

угля на одного рабочего для шахт с

мощностью пласта 8 м и уровнем механизации

работ 6%; найти 95%-ные доверительные

интервалы для индивидуального и среднего

значений сменной добычи угля на 1

рабочего для таких же шахт. Проверить

значимость коэффициентов регрессии и

построить для них 95%-ные доверительные

интервалы. Найти с надежностью 0,95

интервальную оценку для дисперсии

возмущений

.

.

Решение.

В примере 13.4

уравнение

регрессии получено в виде:

.

.

По

условию надо оценить

,

,

где

.

.

Выборочной оценкой ,

,

является

групповая средняя, которую найдем по

уравнению регрессии:

.

.

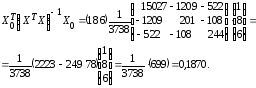

Для построения доверительного

интервала для М (у) необходимо знать

дисперсию его оценки .

.

Для

ее вычисления обратимся к табл. 13.7

(точнее к ее двум последним столбцам,

при составлении которых учтено, что

групповые средние определяются по

полученному уравнению регрессии).

Теперь

по (13.37):

и

(т).

(т).

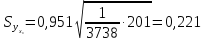

Определяем

стандартную ошибку групповой средней

г> по формуле (13.41).

Вначале

найдем

Теперь

(т).

По

табл. IV приложений при числе степеней

свободы

находим

.

.

По

(13.40)

доверительный

интервал для

,

,

равен

или

или (т).

(т).

Итак,

с надежностью 0,95

средняя

сменная добыча угля на одного рабочего

для шахт с мощностью пласта 8

м

и уровнем механизации работ 6%

находится

в пределах от 4,52

до

6,46

т.

Сравнивая

новый доверительный интервал для функции

регрессии

,

,

полученный

с учетом двух объясняющих переменных,

с аналогичным интервалом с учетом одной

объясняющей переменной (см. пример

13.1),

можно

заметить уменьшение его величины. Это

связано с тем, что включение в модель

новой объясняющей переменной позволяет

несколько повысить точность модели

за счет увеличения взаимосвязи зависимой

и объясняющей переменных (см. ниже).

Найдем

доверительный интервал для индивидуального

значения

при

по

по

(13.43):

(т)

и по (13.42):

,

,

т. е.

(т).

(т).

Итак,

с надежностью 0,95

индивидуальное

значение сменной добычи угля в шахтах

с мощностью пласта 8

м

и уровнем механизации работ 6%

находится

в пределах от 3,05

до

7,93

(т).

Проверим

значимость коэффициентов регрессии

и

.

.

В

примере 13.4

получены

и

.

.

Стандартная

ошибка

в

соответствии с (13.38)

равна:

.

.

Так

как

,

,

то

коэффициент

значим.

Аналогично вычисляем

и

и т.е. коэффициент

т.е. коэффициент

незначим

на 5%-ном уровне.

Доверительный

интервал имеет смысл построить только

для значимого коэффициента регрессии

:

:

по

(13.39)

или

.

.

Итак,

с надежностью 0,95 за счет изменения на

1 м мощности пласта

(при

неизменном

)

)

сменная

добыча угля на одного рабочего У

будет изменяться в пределах от 0,332 до

1,376 т.

Найдем

95%-ный доверительный интервал для

параметра ст2.

Учитывая, что

,

, ,

, найдем по табл.

найдем по табл.

V

приложений при

степенях свободы

степенях свободы ;

; и по формуле(13.43′)

и по формуле(13.43′)

Таким

образом, с надежностью 0,95 дисперсия

возмущений заключена в пределах от

0,565 до 5,35, а их стандартное отклонение

— от 0,751 до 2,31 (т).

Формально

переменные, имеющие незначимые

коэффициенты регрессии, могут быть

исключены из рассмотрения. В экономических

исследованиях исключению переменных

из регрессии должен предшествовать

тщательный качественный

анализ.

Поэтому может оказаться целесообразным

все же оставить в регрессионной модели

одну или несколько объясняющих

переменных, не оказывающих существенного

(значимого) влияния на зависимую

переменную.

Соседние файлы в предмете [НЕСОРТИРОВАННОЕ]

- #

- #

- #

- #

- #

27.03.20162.81 Mб141Учебник Туристское ресурсоведение.rtf

- #

- #

- #

- #

- #

- #

27.03.20164.24 Mб198Физика Яковлев.pdf

Вариации

оценок параметров будут, в конечном

счете, определять точность уравнения

множественной регрессии. Для их измерения

в многомерном регрессионном анализе

рассматривают так называемую

ковариационную

матрицу К,

являющуюся

матричным аналогом дисперсии одной

переменной:

.

где

элементы

ковариации

(или

корреляционные

моменты) оценок

параметров

и.

Ковариация

двух переменных определяется как

математическое ожидание произведения

отклонений этих переменных от их

математических ожиданий [Ссылка]. Поэтому

, (13.28)

где

иматематические

ожидания соответственно для параметров

и

.

Ковариация

характеризует как степень рассеяния

значений двух переменных относительно

их математических ожиданий, так и

взаимосвязь этих переменных.

В

силу того, что оценки

,

полученные методом наименьших квадратов,

являются несмещенными оценками параметров,

т.е.

,

выражение(13.28)

примет

вид:

.

Рассматривая

ковариационную матрицу К,

легко

заметить, что на ее главной диагонали

находятся дисперсии опенок параметров

регрессии, ибо

.

(13.29)

В

сокращенном виде ковариационная матрица

К

имеет

вид:

.

(13.30)

Учитывая

(13.28)

мы

можем записать

.

Тогда

выражение (12.30) примет вид:

,

(13.31)

ибо

элементы матрицы X

—неслучайные

величины.

Матрица

представляет

собой ковариационную матрицу

вектора возмущений

:

в

которой все элементы, не лежащие на

главной диагонали, равны нулю в силу

предпосылки 4

о

некоррелированности возмущений

,

и

между

собой,

а

все элементы, лежащие на главной

диагонали, в силу предпосылок 2

и

3

регрессионного

анализа

равны

одной и той же дисперсии

:

.

Поэтому

матрица

,

где

единичная

матрица

го

порядка.

Следовательно, в силу (13.31)

ковариационная

матрица вектора

оценок

параметров:

Так

как

и

,

то окончательно получим:

(13.32)

Таким

образом, с

помощью обратной матрицынормальных

уравнении регрессии

определяется

не только сам вектор

оценок

параметров (13.28),

но

и дисперсии и ковариации его компонент.

Входящая

в (13.32)

дисперсия

возмущений неизвестна. Заменив ее

выборочной остаточной дисперсией

(13.33)

по

(13.32)

получаем

выборочную оценку ковариационной

матрицы К.

(В

знаменателе выражения (13.33)

стоит

,

а

не

,

как

это было выше в (13.6).

Это

связано с тем, что теперь

степеней

свободы (а не две) теряются при определении

неизвестных параметров, число которых

вместе со свободным членомравно.

4.10. Определение доверительных интервалов для коэффициентов и функции множественной регрессии

Перейдем

теперь к оценке значимости коэффициентов

регрессии

и

построению доверительного интервала

для параметров регрессионной модели

.

В

силу (13.29),

(13.32) и

изложенного выше оценка дисперсии

коэффициента регрессии

определится

по формуле:

где

несмещенная

оценка параметра

;

диагональный

элемент матрицы

.

Среднее

квадратическое отклонение (стандартная

ошибка) коэффициента регрессии

примет

вид:

.

(13.34)

Значимость

коэффициента регрессии

можно

проверить, если учесть, что статистика

имеетраспределение

Стьюдента с

степенями

свободы. Поэтому

значимо

отличается от нуля на уровне

значимости

,

еслисоответствующийныйдоверительный

интервал для параметра

есть

.

(13.35)

Наряду

с интервальным оцениванием коэффициентов

регрессии по (13.35)

весьма

важным для оценки точности определения

зависимой переменной (прогноза) является

построение доверительного

интервала для функции регрессии или

для условного математического

ожидания зависимой переменной

,

найденного в предположении, что

объясняющие переменные

приняли

значения, задаваемые вектором

.Выше

такой интервал получен для уравнения

парной регрессии (см. (13.13)

и

(13.12)).

Обобщая

соответствующие выражения на случай

множественной регрессии, можно получить

доверительный интервал для

:

где

групповая

средняя, определяемая по уравнению

регрессии,

(13.36)

— ее

стандартная ошибка.

При

обобщении формул (13.15)

и

(13.14)

аналогичный

доверительный

интервал для индивидуальных значений

зависимой переменной

примет

вид:

(13.37)

где

.

(13.38)

Доверительный

интервал для дисперсии возмущений

в

множественной регрессии с надежностью

строится аналогично парной модели

по формуле(13.20)

с

соответствующим изменением числа

степеней свободы критерия

:

(13.39)

Пример

13.6.

По

данным примера 13.4

оценить

сменную добычу

угля на одного рабочего для шахт с

мощностью пласта 8 м и уровнем механизации

работ 6%; найти 95%-ные доверительные

интервалы для индивидуального и среднего

значений сменной добычи угля на 1

рабочего для таких же шахт. Проверить

значимость коэффициентов регрессии и

построить для них 95%-ные доверительные

интервалы. Найти с надежностью 0,95

интервальную оценку для дисперсии

возмущений

.

Решение.

В примере 13.4

уравнение

регрессии получено в виде:

.

По

условию надо оценить

,

где

.

Выборочной оценкой,

является

групповая средняя, которую найдем по

уравнению регрессии:

.

Для построения доверительного

интервала для М (у) необходимо знать

дисперсию его оценки.

Для

ее вычисления обратимся к табл. 13.7

(точнее к ее двум последним столбцам,

при составлении которых учтено, что

групповые средние определяются по

полученному уравнению регрессии).

Теперь

по (13.37):

и

(т).

Определяем

стандартную ошибку групповой средней

г> по формуле (13.41).

Вначале

найдем

Теперь

(т).

По

табл. IV приложений при числе степеней

свободы

находим

.

По

(13.40)

доверительный

интервал для

,

равен

или(т).

Итак,

с надежностью 0,95

средняя

сменная добыча угля на одного рабочего

для шахт с мощностью пласта 8

м

и уровнем механизации работ 6%

находится

в пределах от 4,52

до

6,46

т.

Сравнивая

новый доверительный интервал для функции

регрессии

,

полученный

с учетом двух объясняющих переменных,

с аналогичным интервалом с учетом одной

объясняющей переменной (см. пример

13.1),

можно

заметить уменьшение его величины. Это

связано с тем, что включение в модель

новой объясняющей переменной позволяет

несколько повысить точность модели

за счет увеличения взаимосвязи зависимой

и объясняющей переменных (см. ниже).

Найдем

доверительный интервал для индивидуального

значения

при

по

(13.43):

(т)

и по (13.42):

,

т. е.

(т).

Итак,

с надежностью 0,95

индивидуальное

значение сменной добычи угля в шахтах

с мощностью пласта 8

м

и уровнем механизации работ 6%

находится

в пределах от 3,05

до

7,93

(т).

Проверим

значимость коэффициентов регрессии

и

.

В

примере 13.4

получены

и

.

Стандартная

ошибка

в

соответствии с (13.38)

равна:

.

Так

как

,

то

коэффициент

значим.

Аналогично вычисляем

ит.е. коэффициент

незначим

на 5%-ном уровне.

Доверительный

интервал имеет смысл построить только

для значимого коэффициента регрессии

:

по

(13.39)

или

.

Итак,

с надежностью 0,95 за счет изменения на

1 м мощности пласта

(при

неизменном

)

сменная

добыча угля на одного рабочего У

будет изменяться в пределах от 0,332 до

1,376 т.

Найдем

95%-ный доверительный интервал для

параметра ст2.

Учитывая, что

,,найдем по табл.

V

приложений при

степенях свободы;и по формуле(13.43′)

Таким

образом, с надежностью 0,95 дисперсия

возмущений заключена в пределах от

0,565 до 5,35, а их стандартное отклонение

— от 0,751 до 2,31 (т).

Формально

переменные, имеющие незначимые

коэффициенты регрессии, могут быть

исключены из рассмотрения. В экономических

исследованиях исключению переменных

из регрессии должен предшествовать

тщательный качественный

анализ.

Поэтому может оказаться целесообразным

все же оставить в регрессионной модели

одну или несколько объясняющих

переменных, не оказывающих существенного

(значимого) влияния на зависимую

переменную.

Соседние файлы в предмете [НЕСОРТИРОВАННОЕ]

- #

- #

- #

- #

- #

27.03.20162.81 Mб141Учебник Туристское ресурсоведение.rtf

- #

- #

- #

- #

- #

- #

27.03.20164.24 Mб196Физика Яковлев.pdf

Battery state-of-power evaluation methods

Shunli Wang, … Zonghai Chen, in Battery System Modeling, 2021

7.4.4 Main charge-discharge condition test

The initial value of the error covariance matrix P0 can be determined from the X0 error of the initial state. In the application, the initial value should be as small as possible to speed up the tracking speed of the algorithm. Two important parameters are processed noise variance matrix Q and observation noise variance matrix R. As can be known from theoretical formula derivation, the dispose to Q and R plays a key role in improving the estimation effect by using this algorithm. Because it affects the size of the Kalman gain matrix K directly, the value of error covariance matrix P can be described as shown in Eq. (7.61):

(7.61)Rk=Eυk2=συ2

It is the expression of the observation noise variance, which is mainly derived from the distribution of observation error of experimental instruments and sensors, as shown in Eq. (7.62):

(7.62)Qk=Eω1k2Eω1kω2kEω2kω1kEω2k2=σω1,12σω1,22σω2,12σω2,22

It is the relationship between the system noise variance and the processing noise covariance. The two states in the system are generally unrelated and the covariance value is zero. Therefore, the diagonal variance can have a small value. The variance Q of processing noise is mainly derived from the error of the established equivalent model, which is difficult to be obtained by theoretical methods or means. A reasonable value range can be obtained through continuous debugging through simulation, and it is usually a small amount.

To verify the applicable range and stability of the algorithm, the input of different working conditions is used to observe the estimation accuracy of the algorithm. In this simulation, two working conditions are used: the constant-current working condition and the Beijing bus dynamic street test working condition. For the constant-current condition, only a constant value needs to be set in the program. To increase the complexity of the condition, two shelved stages are added to the constant-current input list to verify the tracking effect of Ah and the extended Kalman filtering. The following code is generated for the current.

The experimental data should be used to simulate the algorithm under its operating conditions. The current input module is realized in the environment under Beijing bus dynamic street test operating conditions. It is the time integration module, whose output is the capacity change of the working condition, and the lower part is the working condition data output module. It outputs the current into the workspace at the minimum time interval of the sampling measurement. The data onto the workspace are a time-series type and the current data need to be extracted. The data extraction and transformation can be performed in the main program, wherein the working condition is the Simulink module. The current is the time-series data, including the current output. S_Est is the algorithm program module, whose input is the initial S_Est_init and current data onto the estimated state value.

The current data are input into the program module of the extended Kalman filtering algorithm based on the model, and the initial values of other parameters have been determined in the program. The program finally outputs the ampere hour time integral and the state estimation curve of the extended Kalman filtering through the minimum time interval of 10 times as the sampling time. The current curve of the experimental test can be obtained as shown in Fig. 7.13.

Fig. 7.13. Pulse current operating current curve for the experimental test. (A) Main charge working condition. (B) Main discharge experimental test.

The unscented Kalman filtering algorithm is programmed by writing scripts to realize algorithm simulation to compare the output effect. The specific implementation process conforms to the processing requirements, and the main simulation program can be constructed. The program takes 10 times the minimum time interval as the sampling time and simulates the three methods of the state estimation, including ampere hour time integration, extended Kalman filtering, and unscented Kalman filtering, to compare the following situation of the three methods of the state over time. The program simultaneously outputs the state variation curve and estimation error curve with time, so that the tracking effect and error variation on the three methods can be obtained visually. Its implementation process is consistent with script. Different modules are used to replace the code block. The integration advantage of the environment is used in the graphical interface to obtain the same stimulation effect.

The operation logic is ensured by the unchanged intuitive presentation of the calculation process. Based on script implementation, the modular simulation is built accordingly. The experiment data are used as the input current, and the state prediction is obtained by the state prediction module. The forecast and model parameters are calculated. After that, the equivalent model can be used to predict the completion status value of Up as well as the output voltage. The input of the algorithm includes the update module, output state correction, and error covariance matrix update as the basis of the forecast. It takes the ampere hour integral result as the minimum time interval of the current data, which is taken as the reference value of the measured state.

The estimation effect of ampere hour and extended Kalman filtering is compared when the minimum time interval can be set as 10 times as the sampling period. The stability of the extended Kalman filtering algorithm is evaluated under working conditions. The state variable needs to accept the last estimated value as the basis of the next state prediction, in which the predicted value Up_pre is directly input into the corresponding position of the resistance-capacitance circuit modeling to conduct the terminal voltage prediction of the current polarization voltage. The functions of each part are realized in a more modular way for the complete structure and clear hierarchy.

Read full chapter

URL:

https://www.sciencedirect.com/science/article/pii/B9780323904728000044

Dynamic Model Development

P.W. Oxby, … T.A. Duever, in Computer Aided Chemical Engineering, 2003

3.2 An Optimality Property of the Determinant Criterion

Equation (12) can be generalized by replacing the inverse of the estimate of the error covariance matrix,

Σ^εn−1, with an arbitrary symmetric positive definite weight matrix, W:

(14)Δθ^(k)=(XTWX)−1XTWz(θ^(k))

The estimate of the parameter covariance is:

(15)Σ^θ=(XTWX)−1XTWΣ^εn(XTWX)−1

If the determinant of the estimate of the parameter covariance matrix,

|Σ^θ|, is minimized with respect to the elements of W, the solution is independent of X and is simply

(16)W=Σ^εn−1

Substitution of (16) back into (14) gives (12) which, as has been shown, is equivalent to the determinant criterion. Therefore of all weighting schemes in the form of (14), it is the one equivalent to the determinant criterion that minimizes

|Σ^θ|, the determinant of the estimate of the parameter covariance matrix when the error covariance is unknown. This appears to be a rather strong result in support of the determinant criterion. It might also be noted that, unlike derivations based on likelihood, this result does not depend on the measurement errors being normally distributed. But it will be shown that the practical usefulness of the result does depend on the assumption that the residual covariance